Purchasing a residential property is one of the significant financial decisions in one’s life. Along with the exponential rise in the real estate sector, there is a steady growth of home loans in the financial market as well. India’s leading financial institutions and NBFCs are cashing in on this real estate boom by providing borrower-friendly home loans to help prospective buyers make their necessary purchase.

However, most borrowers are unaware of the formalities they need to fulfil their housing loan approved. Henceforth, individuals who want to avail a home loan must stay aware of some aspects before making the purchase.

Here are some of the tips to follow before opting for a housing loan –

Tip 1: Credit score

CIBIL score is one of the crucial factors taken into consideration by the financial institutions before providing any advances to its customers. So, prospective borrowers need to hold a good credit score of 750 or more with a clean repayment track record.

This will not only improve your home loan eligibility criteria but also earn you a better interest rate as well. It instils a sense of confidence among the lenders that you can repay the loan without defaulting.

Tip 2: Rate of interest

Every loan seeker must compare the interest rates of different lenders and settle on one that offers the lowest home loan interest rate. Rate of interest plays a pivotal role in determining the affordability of a financial advance.

Furthermore, borrowers can choose between two types of interest rates – fixed or floating. Under a fixed home loan interest rate, the rate is immune to market fluctuations. Therefore, your monthly pay-outs will not vary throughout the loan tenure.

On the other hand, the interest rate under floating is calculated regarding its change with the market fluctuations. It is recommended to go for floating rates as it might prove beneficial in the future when the rate drops.

Tip 3: Loan tenure

Any individual who considers availing a home loan must decide on the loan tenure as your equated monthly instalments are directly available on it. Lending institutions prefer to sanction advances with an extended tenure for the convenience of borrowers and to earn revenue from interests. So, if you have a stable income or surplus cash in hand – opt for a shorter tenure as it lowers the interest burden on the EMIs. Although it increases your monthly outgo, it also reduces the total cost of loan significantly in the longer run.

Tip 4: Consider the fees involved

When you opt for a home loan, you need to pay a processing fee to your lender once your application is accepted. Also, keep in mind the associated charges or fees involved on a pre-payment, foreclosure or late payment penalty. These charges are even more important to consider if you plan to complete the loan repayment before the loan tenure. Hence, opt for lenders that offer zero part-prepayment and pre-closure charges.

Tips 5: Documents required for a home loan

This is a list of all documents required for a home loan in India –

-

Identity and address proof like Voter ID card, PAN card, Aadhaar card, Passport, etc.

-

Property documents both in photocopies and documents.

-

Income proof such as salary slips, bank account statements, income tax returns.

-

Proof of your employment stability like appointment letter, increment slips, etc.

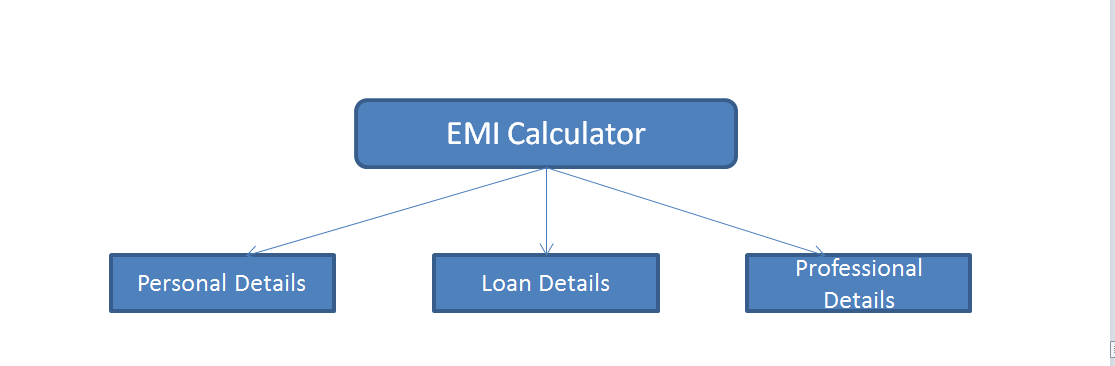

Equipped with this information related to tips before opting for a home loan, you can calculate home loan eligibility before availing such credit. By putting all the required details, check, if you qualify for this credit facility and apply with confidence.

You can consider availing a Home Loan from lenders like Bajaj Finserv who offer numerous borrower-friendly and industry-first features. They also bring you various offers for their existing customers.

Refer to such leading lenders to easily repay your home loan and ease the loan repayment burden. Manage your finances effectively and go ahead with a part prepayment or even a foreclosure to reduce the total EMIs you are liable to repay.